That isn’t just the circumstances if you are intending to get a separate house security mortgage or credit line (HELOC). For many who curently have a good HELOC otherwise financing that have a varying interest, that’s going to increase.

New Given last week revealed it can boost its standard quick-label rate of interest brand new government fund price of the 75 foundation situations as an element of the constant bid so you can rein into the continually large inflation. Rates had been 8.3% large for the August than they were a year prior to, according to Agency out of Work Statistics, that was higher than expected.

One increase in this new government loans rates was designed to discourage spending and remind rescuing, planning to offer cost down.

Rising prices was a primary concern for all those, claims Brian Walsh, senior movie director regarding economic think during the SoFi, a national personal fund and you will lending company. It has an effect on anyone and it’s especially harmful to people on the entry level of the money range. The newest Fed should score inflation in control and they’ve got relatively restricted devices to accomplish this. Should it be finest or perhaps not, they have to explore their tools on their disposal. One of the many of these was elevating pricing.

A higher government finance rate would mean higher rates of interest to have a myriad of financing, and it’ll features an exceptionally lead influence on HELOCs and you will almost every other issues with adjustable costs you to move around in show toward main bank’s transform.

In whatever way your make the grade, it’s not going to getting fun to possess a top commission every month on the same amount of money, states Isabel Barrow, manager regarding financial thought from the Edelman Financial Motors, a nationwide financial planning organization.

How Such Pricing Are Calculated

This type of prices are from a survey presented of the Bankrate, which such as for example NextAdvisor try owned by Red Options. The fresh averages have decided of a study of one’s top 10 banking institutions regarding the top You.S. places.

Exactly how Have a tendency to new Fed’s Rates Hike Apply to Home Guarantee Financing and you may HELOCs?

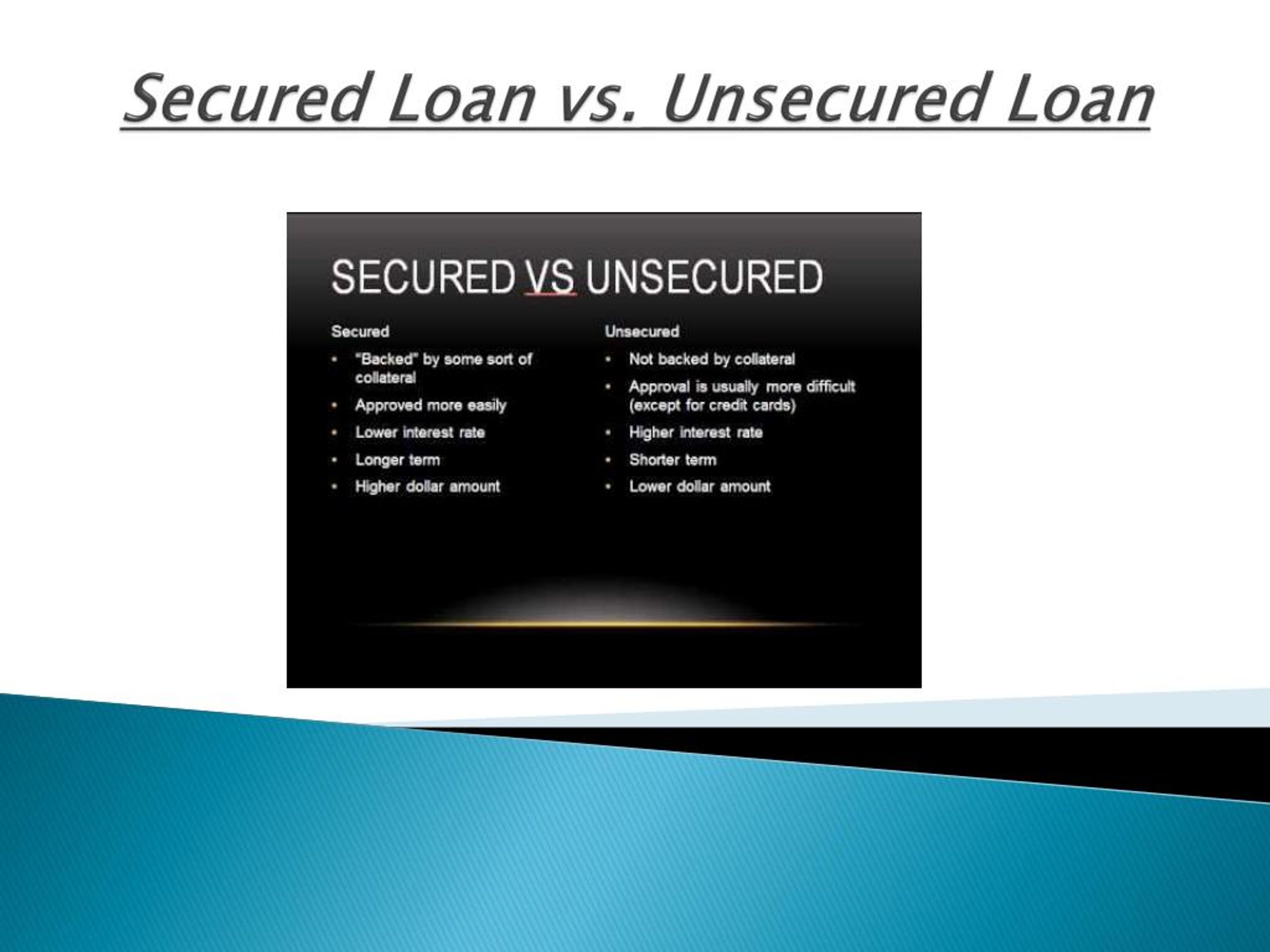

Family security funds and HELOCs try equivalent. Make use of the payday loan Centennial latest security of your property – the essential difference between its well worth and you may your balance on your mortgage or other home loans – as collateral discover a loan. This means otherwise pay it back, the financial institution can also be foreclose on your domestic.

Household equity money

House equity loans are often quite straightforward, for the reason that you obtain an appartment amount of cash initial and you may after that pay it off more than a flat long-time during the a fixed interest. The latest pricing for household collateral money are based on your own credit chance while the pricing towards financial to get into the bucks needed.

The brand new Fed’s benchmark price is actually an initial-title one that affects what banks charges both so you’re able to obtain money. You to definitely walk tend to boost charges for financial institutions, probably riding higher interest rates towards items like home guarantee finance.

Rates to own house equity funds tend to be a tiny bit more than to have HELOCs, but that’s as they tend to have fixed costs. You aren’t using exposure you to rates commonly upsurge in the latest upcoming because they likely tend to. You pay a little bit more into the need for buy discover that risk mitigation, Barrow says.

HELOCs

HELOCs are like a credit card secure by your home equity. You have a threshold of simply how much you could potentially obtain during the one-time, but you can use some, repay it, and you can borrow a great deal more. You are able to pay only interest about what you acquire, but the interest rate is variable, altering regularly since field rates changes.